Technology companies have an enormous opportunity to capitalize on the many intangible assets they create. These include intellectual property (IP) rights such as patents, copyrights, trademarks and trade secrets, as well as other assets including data, brand reputation, strategies, and customer and business relationships.

As technology companies develop new products and services, however, these processes and intangible asset portfolios require close assessment and management.  Organisations often struggle to balance the development of new products and features with maintaining the reliability of their systems. Heightened demand for digital services during the coronavirus pandemic means businesses must urgently assess the consequences on their IT systems of any such changes, so that they can protect continuity and empower sales growth.

The insurance industry could face a public relations disaster if it maintains an across-the-board stance of rejecting claims under business interruption policies during the coronavirus pandemic. The situation appears to be worsening thanks to the actions of several firms that have clear terms including pandemic coverage, but which are nevertheless refusing to pay apparently valid claims.

Digital channels have long been reshaping our human connections, but the coronavirus crisis means businesses are suddenly faced with a new reality: a near-total reliance on online communications. This is prompting a deeper and nuanced social-first approach.

The coronavirus crisis has created an acutely uncertain environment for businesses. Many are using physical assets to access the working capital needed to survive. But what about businesses whose rapid growth is driven by intangible assets?

Cars are becoming increasingly autonomous, with manufacturers moving ever closer towards fully driverless vehicles. For the insurance industry, the potential ramifications are transformational.

In view of this change, insurers clearly need to address some questions. First, who will be accountable in the case of accidents involving driverless vehicles? And will anyone need car insurance when they are not actually drivers of their vehicles?  Sanctions have long been a serious concern for banks. However, they are now being applied more regularly across a variety of industries. Breaking them can quickly lead to heavy fines, export bans, denial of access to the US banking system, reputational damage, and severe supply chain disruption. Individuals involved risk criminal charges.

Amidst great macroeconomic uncertainty during the coronavirus outbreak, banks are also facing immense pressure from stringent regulations. Among the most pressing and potentially impactful of these regulations is IFRS 9. Institutions must now spot signs of danger in their loan portfolios at a much earlier stage, requiring deep operational and strategic changes.

The last major financial marketplace to be transformed by technology is the corporate bond market, but a new online trading venue is now providing access to fixed income in affordable sizes.

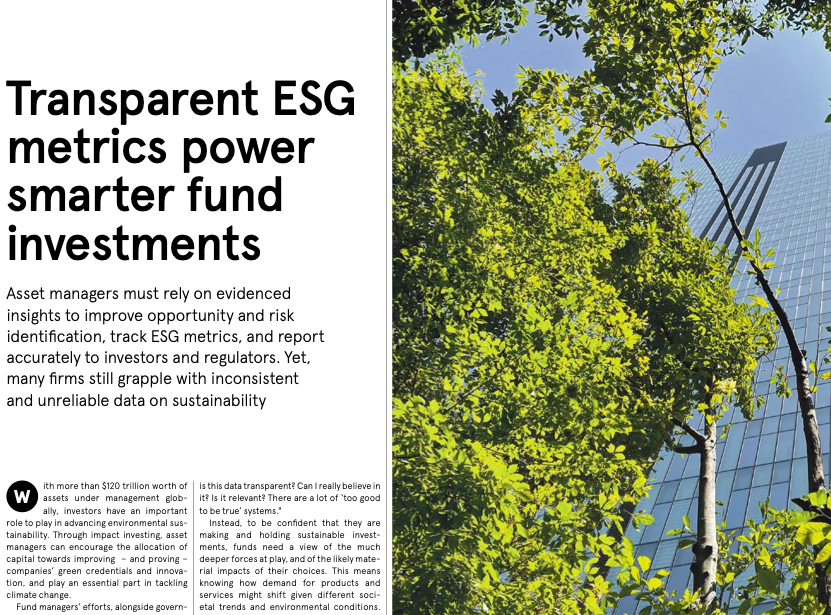

This sudden liberalisation of the main corporate bond markets amounts to something of a revolution. While in the UK, 53 per cent of pension investments go into bonds, direct investment by individual investors in corporate bonds remains negligible. With equity trading becoming more volatile, access to corporate bonds gives investors a means to buy in to established companies with reliable returns.  A significant shift is gathering momentum in the Life Sciences and Healthcare industry. Return on investment from late‐stage pipelines in Big Pharma is at an all‐time low. The pressure to increase returns is driving a sharpened focus on reducing time to market. Faster drug development is being enabled through advances in data capture and analytics.

|

Recent portfolioA selection of articles, reports and other content. Archives

February 2024

Categories

All

|

RSS Feed

RSS Feed